During the first quarter, investors wavered from euphoria to despair, as record market gains in January were followed by the first “corrections” (drops of 10% from record highs) in February in more than 2 years. The Dow and S&P 500 closed out the month of March and first quarter with declines, breaking a streak of nine consecutive winning quarters. Volatility, which had long been dormant, roared back to life during the quarter, as the VIX (commonly known as the “fear index”) posted its biggest quarterly rise – up 81%.

One of the primary drivers for the markets’ decline were concerns that wage growth may indicate a return of inflation, and subsequent further and more frequent interest rate hikes by the Federal Reserve. The Fed raised interest rates at its March meeting, and indicated at least two more hikes this year and more in 2019 and 2020. Additionally, trade war fears intensified after proposed tariffs and steel and aluminum imports from non-North American countries and technology tariffs targeted on China.

The market’s decline was widespread, as nine of the eleven S&P sectors posted negative returns for the quarter. The only two sectors that were positive were Technology (2.3%) and Consumer Discretionary (2.6%), sectors which benefited from the FAANG stocks (Facebook, Apple, Amazon, Netflix, and Google). The worst performing sectors were Consumer Staples (-7.5%), Energy (-6.7%), and Materials (-5.9%).

During the quarter the bond market faced disaster, as prices for both short and long term issues tanked, sending yields soaring on the fear of re-emerging inflation. The yield on the 10-year hit a four-year intraday high of 2.95% in February. The concern over protectionist tariffs and subsequent market volatility drove investors to safe haven assets like bonds, which drove yields lower in March. The current yield on the 10-year is 2.74%.

Oil prices ended higher, with West Texas Intermediate crude settling at $64.64 a barrel, posting its third straight quarterly rise in a row. Geopolitical concerns and possible actions by OPEC countries to trigger higher prices may generate further increases.

Economic indicators showed mixed results. The Chicago PMI slipped to 57.1 from 61.9 in February, showing continued softening in business sentiment. However, any reading above 50 indicates improving conditions. Consumer confidence fell to 127.7 in March from 130.0 in February, which was an 18-year high. Unemployment remains at 4.1%, a 17-year low. The Consumer Price Index for All Urban Consumers (CPI-U) rose 0.2% in February on a seasonally adjusted basis. Over the last 12 months, the all-items index rose 2.2 percent. On the whole, these numbers reflect a healthy economy and support further interest rate increases.

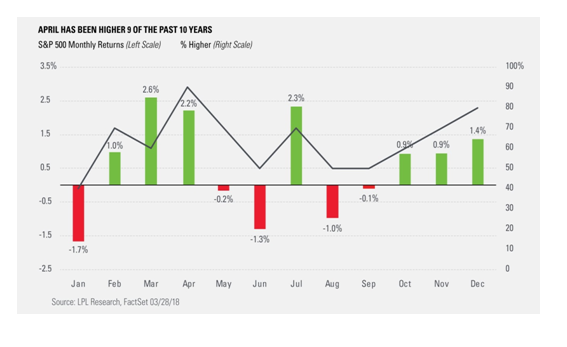

The quarter certainly showed that risks are still present in the markets. But if it is of any comfort to know, according to the Stock Trader’s Almanac, April has historically been the strongest month for the Dow, with average gains of 1.9%, based on data going back to 1950. April has been the third best month for the S&P 500 and Russell 2000, with average gains of 1.5% for both indices (see chart).

While those average returns would be much-welcomed, they would not bring the indices back to the record territories we witnessed earlier this year. Investors should remain focused on the long-term, and confirm that their risk tolerance matches the potential volatility we may see ahead.